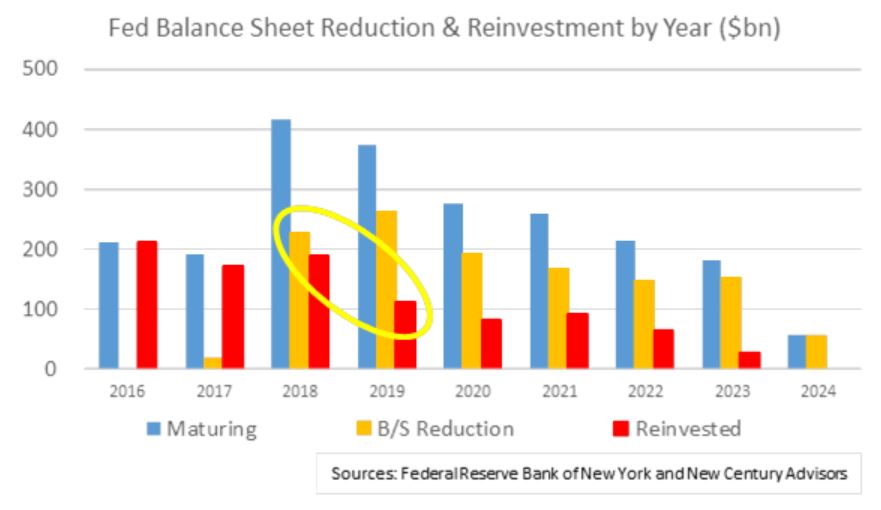

Despite balance sheet reduction, the Fed actually bought MORE Treasuries in 2018 vs. 2017. That reverses direction in 2019 when the Fed will be buying just $112.2bn, down from $187.7bn last year. And that’s not even mentioning increased issuance. #Fed #Rates #Treasury

Important Disclosures: PAST PERFORMANCE IS NOT AN INDICATOR OF FUTURE RESULTS. Forward looking statements: Any projections, forecasts and estimates contained herein are forward looking statements and are based upon certain assumptions that New Century Advisors considers reasonable. Projections are necessarily speculative in nature, and it can be expected that some or all of the assumptions underlying the projections will not materialize or will vary significantly from actual results. Accordingly, the projections are only an estimate. Actual results may vary from the projections, and the variations may be material. Some important factors that could cause actual results to differ materially from those in any forward looking statements include changes in interest rates, market, financial or legal uncertainties, the timing of acquisitions of the underlying assets, the timing and frequency of defaults on the underlying assets, amongst others. Consequently, the inclusion of projections herein should not be regarded as a representation by the manager of the results that will actually be achieved. New Century Advisors, LLC has no obligation to update or otherwise revise any projections, including any revisions to reflect changes in economic conditions or other circumstances arising after the date hereof or to reflect the occurrence of unanticipated events, even if the underlying assumptions do not come to fruition. The securities listed in New Perspectives are not to be considered recommendations or an offer to buy or sell securities and are being used as illustrations only. Past performance is not an indicator of future results. There is no guarantee that the investment objective of the strategy will be achieved. Index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. One cannot invest directly in an index. CLIENTS MUST BE PREPARED TO BEAR THE RISK OF A TOTAL LOSS OF THEIR INVESTMENT. THE THEMES AND STRATEGIES HEREIN ARE NOT TO BE CONSTRUED AS RECOMMENDATIONS. THEY ARE FOR ILLUSTRATION PURPOSES ONLY AND SUBJECT TO CHANGE WITHOUT NOTICE.

Data provided by New Century Advisors, LLC and the Federal Reserve Bank of New York. NCA does not guarantee or warrant the accuracy, timeliness, or completeness of third party provided information and is not responsible for any errors or omissions. The discussion of any investments in this presentation is for illustrative purposes only and there is no assurance that the adviser will make any investments with the same or similar characteristics as any investments presented. The investments identified and described do not represent all of the investments purchased or sold for client accounts. The representative investments discussed were selected based on a number of factors including, investment process and subject matter applicability. The reader should not assume that an investment identified was or will be profitable. The information contained in this email or document may not be reproduced or provided to others without the prior written permission of New Century Advisors, LLC. The information provided is neither an offering nor a solicitation of an offering for any securities. Nothing contained herein shall constitute any representation or warranty as to future performance.